The Common Reporting Standard (CRS) is a global standard for the automatic exchange of financial account information between tax authorities of different countries. The CRS was developed by the Organization for Economic Co-operation and Development (OECD) and endorsed by the G20 in 2014.

The CRS requires financial institutions, such as banks, to identify and report information on foreign account holders to their local tax authorities, who then exchange the information with the tax authorities of other participating countries. The information reported includes the account holder’s name, address, tax identification number, and details of their financial accounts, including balances and income.

The objective of the CRS is to promote tax transparency and combat tax evasion by ensuring that taxpayers cannot hide assets or income in offshore accounts without detection. The standard has been adopted by more than 100 jurisdictions worldwide, making it the global standard for the automatic exchange of financial account information.

Participating countries are required to implement the CRS through domestic legislation, which sets out the rules and procedures for the exchange of information. The standard also includes provisions for the confidentiality and protection of exchanged information, and provides a legal framework for the exchange of information between participating countries.

Overall, the CRS is an important tool for promoting tax transparency and cooperation between countries, and has been successful in increasing the exchange of information on financial accounts and assets held offshore.

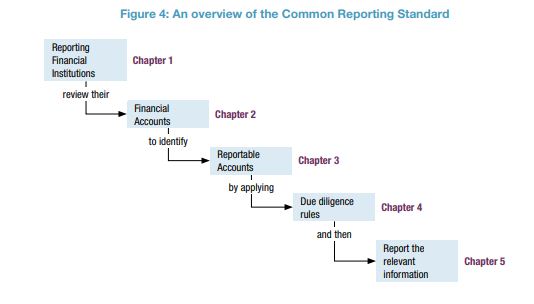

An overview of the Common Reporting Standard

The central part to the Standard is the CRS, which contains the detailed rules and procedures that financial institutions must follow in order to ensure the relevant information is collected and reported. It is these rules that must be incorporated into domestic law to ensure the due diligence and reporting is performed correctly. Conceptually, the CRS can be broken down into a number of steps, each of which is analysed in turn throughout the remainder of the Handbook. The steps are depicted in Figure 4, which also shows the Chapters that contain the discussion on each step

Also read : GAAR